THE COMPETITIVE ADVANTAGE OF REGIONAL AIRCRAFT

24

24

)

2017 was a different time. Barely five years past, the intense competition for the business passenger seems a story for a bygone era.

In the world’s largest market, the fight amongst the U.S. network airlines was for the high yield passenger. Increasing connectivity brought new corporate accounts, higher fares, and increased profitability. There was no better place to find these advantages than in the regional networks.

REGIONAL CONNECTIVITY SURVIVES AND THRIVES

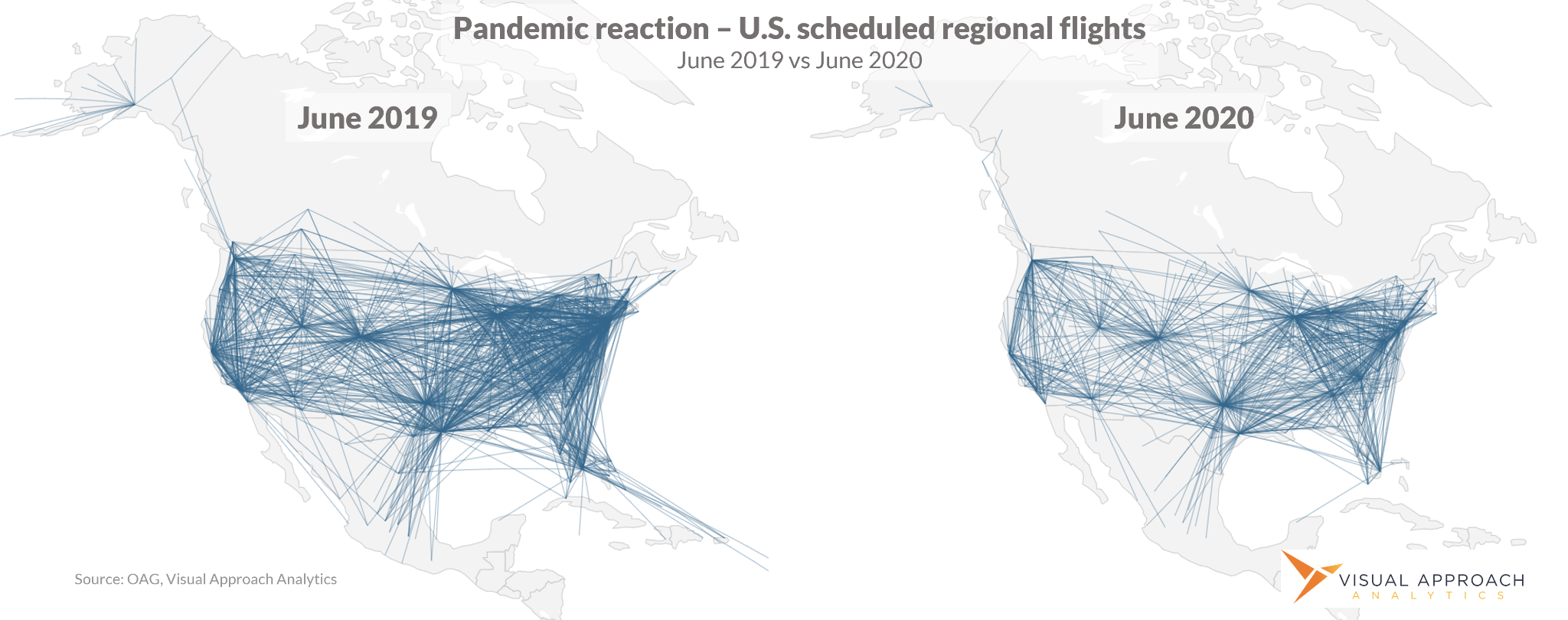

In April of 2017, United Airlines made a decisive move to increase its competitive network by adding 65 50-seat CRJ200 aircraft from Air Wisconsin to its United Express fleet. Contrary to the long-expected sunset of the 50-seat jet, the ability for the aircraft to increase connectivity through United’s Chicago and Washington D.C. hubs proved critical in the fight for the business passenger. The fight for the business passenger, network connectivity, and higher fares reached a fever pitch.Of course, March 2020 changed everything. The idea of optimizing revenue on full aircraft gave way to empty seats and a scramble to save costs. Even as the first signs of the recovery started to appear in Summer 2020, the business traveler was nowhere to be found. Leisure travel ruled the skies, and the airline networks adjusted quickly to accommodate. Today, regional connectivity continues, even without the highly sought-for business passenger who so demanded the service.

It is through the lens of connectivity, and the competitive advantages which were once so highly sought, that we assess the impact of the regional aircraft through the drastic changes of the pandemic.

Beyond the fact that regional aviation was able to maintain connectivity during the most difficult times, and even though we are in an early recovery phase today, we now look to the future, and how regional aviation is expected to, once again, become the competitive differentiator in the United States.

A NEW NICHE FOR REGIONAL FLEETS

For airlines around the world, the objective of Spring 2020 was brutally simple - survive. As air travel plummeted 97% in April, entire fleets of aircraft were parked in a bid to save precious cash. As larger mainline aircraft which remained active found themselves flying with mostly-empty seats, the protective role of the country’s regional aviation network became apparent

Despite the unprecedented drop in travel demand, the air transportation system in the United States maintained its connective integrity, driven largely by a regional fleet. Yet, as critical as this essential service of maintaining connectivity amid a crisis may be, it is not the core role of regional aviation. Regional aviation exists to compound airline presence, to be a competitive instrument, and most importantly, to be profitable.

Even as the demographic of the U.S. domestic traveler has become increasingly leisure-oriented, so too have the networks shifted to larger aircraft in order to connect many vacationers with the few vacationheavy destinations. Tourist destinations such as Florida, Colorado, and Las Vegas saw robust recoveries, driven by larger jets full of passengers paying low fares. Meanwhile, the high-yield business traveler remains elusive.

For a regional industry so dependent upon the value brought from connectivity rather than simply discounted fares, the slow return of the business traveler might seem concerning. However, no evidence suggests that ultra-low business travel is here to stay.

Leisure demand has recovered, fulfilling much of the demand present prior to the pandemic. However, the long-awaited real recovery is expected to be business and international demand-driven, where the greatest opportunity for regrowth remains.

Analysis of market concentration strongly suggests that the regional aircraft in the United States will once again signal a strong competitive advantage, just as it did in 2017.

This anticipated growth in business and international demand is highly dependent upon network connectivity - precisely the competitive advantage brought by a robust regional network.

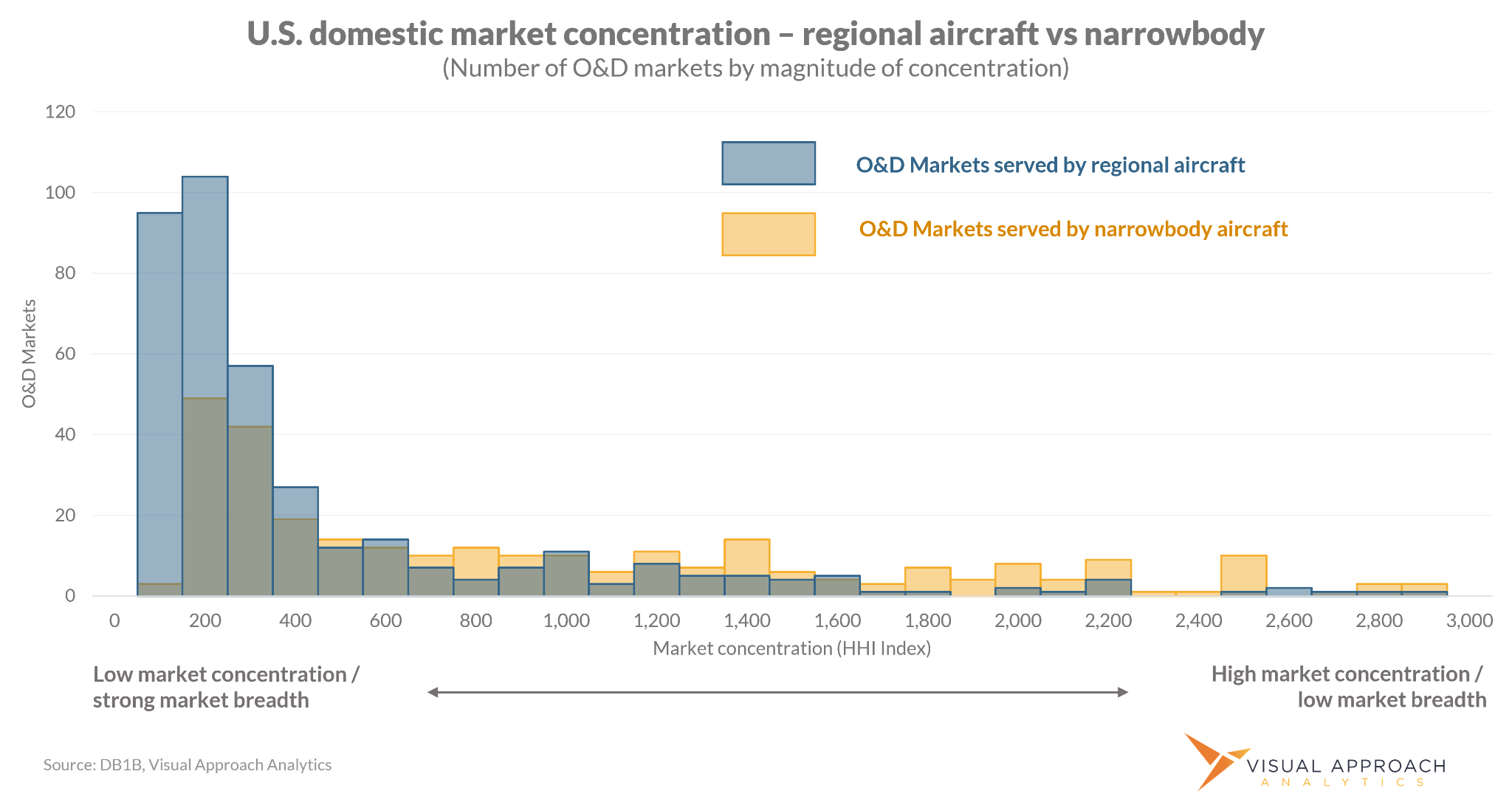

The breadth of an airline’s network can be best described by its market concentration. The higher the market concentration, the more passengers will be required to find alternative airports to complete their travel. This becomes critical for small and medium-sized communities where larger aircraft may fly to the vacation hot-spot; however, any other travel requires a drive to the larger airport.As such, the competitive nature of a market to capture the business traveler for an airline can be illustrated by market concentration. To measure concentration, we use the Herfindahl-Herschman Index (HHI), a long-standing metric comparing the market size to the market breadth. In the context of air travel, a higher HHI indicates passenger traffic with few options, whereas a low HHI indicates strong market breadth and a diversified network.Whencomparing HHI values of actual itineraries flown during Q2 2021, the competitive nature of the regional network stands out. In markets where regional jets were a part of the itinerary, market concentration was one-fourth of the itineraries operated by narrowbody aircraft. This staggering increase in market breadth the regional aircraft illustrates just how competitive a full network can be, once travel expands beyond the few leisure destinations.

MORE PASSENGERS RELYING ON REGIONAL AVIATION

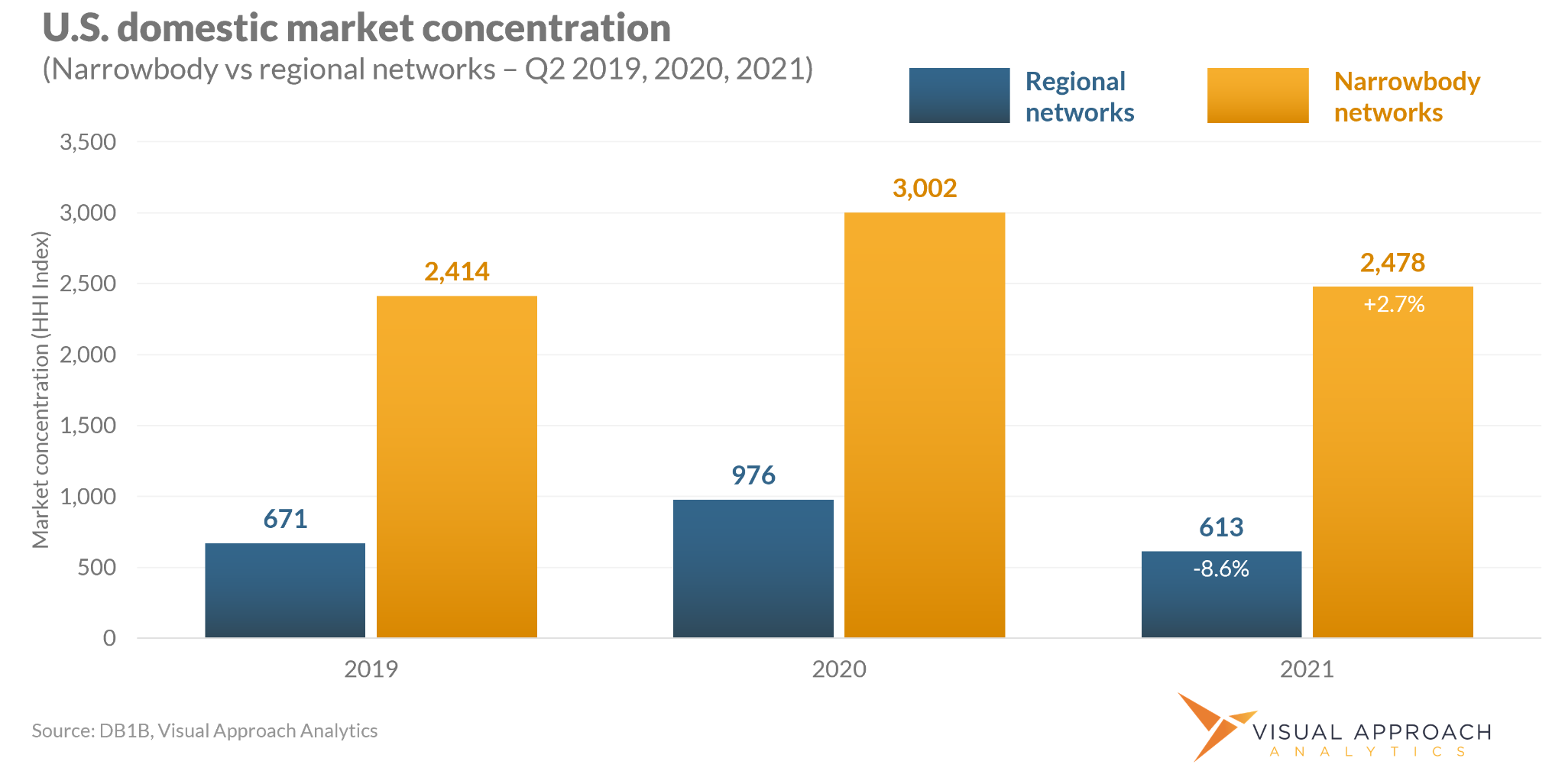

Over the course of the pandemic, the market concentration for narrowbody aircraft has further increased, reflecting the increasing leisure demand and fewer connecting options. Compared to 2019, narrowbody networks have increased network concentration by 2.7%.

Conversely, the reliance on the regional aircraft to maintain a competitive network has increased. Market concentration of itineraries involving regional aircraft fell by almost 9% since 2019, showing how much more passengers rely on regional aviation to travel to all but the most popular destinations.

PREPARING FOR BUSINESS TRAVEL GROWTH

Today, with the recovery in the high-value business and international traveler just beginning, this competitive network advantage the regional airlines bring has not yet been realized. Further, a pilot shortage impacting the regional airlines is putting pressure on available capacity to maintain this low concentration and high market breadth.

These two factors are working together to create a shift toward the leisure passengers who have returned, at the risk of not being competitive for the business travelers who are about to return.The result is difficult to see from within a currently depressed business travel environment, however, the airlines which maintain and grow their regional networks today will be in a position to corner the business travel market tomorrow.

Just as network connectivity was paramount in 2017, so too will it be paramount as the recovery continues. Market concentration for larger aircraft continues to increase, but it is up to the regional networks, which have increasingly been relied upon, to maintain a connection to the world’s air transportation system. The competitive advantages are only set to continue.

We are happy to bring you this special contribution from Courtney Miller, Founder and Managing Partner of Visual Approach. Courtney has over 20 years of aviation analysis experience. A particularly talented storyteller, he finds insights and trends in the aircraft, network, and financial segments of the industry and presents them in an intuitive way. His data and analysis can be seen regularly in The Air Current and Cranky Network Weekly. You can contact him at: courtney@visualapproach.io, and learn more about Visual Approach Analytics at: https://visualapproach.io.

Contributor: Courtney Miller, Founder and Managing Partner of Visual Approach

- Log in to post comments